Table of Content

On average, our heroes save over $3,000 when they buy, sell or refinance a home with our local specialists.

The chart below lists common loan types and the basic (and wide-ranging) requirements for each. In the DTI ratio column, where two figures appear, the first refers to housing-only debt and the second refers to all debt. Under PMI/MIP /Fee, two numbers separated by a slash (/) indicate an up-front fee followed by an annual fee . All mortgage loans have additional requirements not listed here. Your DTI ratio measures all of your monthly debts relative to your monthly income.

Pre qualified vs Pre approved | What does Pre-Approved Mean for a Mortgage?

The faster you send them in, the sooner your mortgage can be approved. A home buyer’s ability to repay its mortgage gets based on Debt-to-Income. The best time to get pre-approved for a mortgage is at least one year before you decide to purchase. The difference between a pre-approval and pre-qualification is that mortgage pre-approvals get used to buy a home – pre-approval cannot. So, if you’re serious about buying a home, here’s how to get pre-approved for a mortgage.

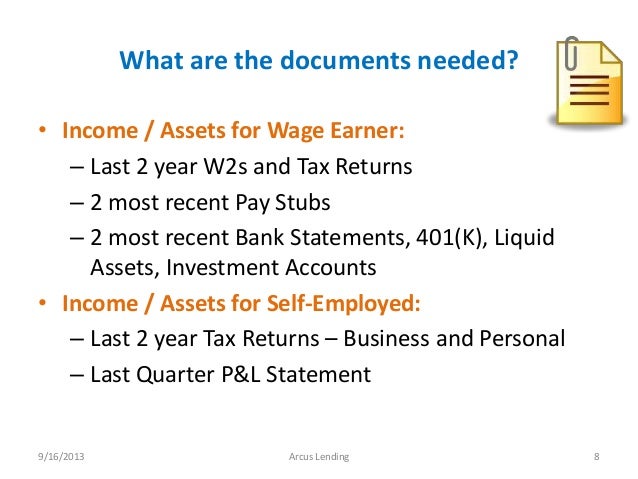

Opinions expressed here are author's alone, not those of any bank, credit card issuer or other company, and have not been reviewed, approved or otherwise endorsed by any of these entities. All information, including rates and fees, are accurate as of the date of publication and are updated as provided by our partners. Some of the offers on this page may not be available through our website. After selecting a lender, the next step is to complete a full mortgage loan application. Most of this application process was completed during the pre-approval stage. But a few additional documents will now be needed to get a loan file through underwriting.

How to Get a Loan for a House Without a Co-signer

We’ll do a full verification of your income, assets and credit so sellers can be certain you won’t run into financing issues. Preapproval and prequalification are both ways of understanding how much you’ll be able to get approved for. There are some slight differences between these two processes, though some lenders use these terms interchangeably. A mortgage application is submitted to a lender when you apply for a loan and includes information that determines whether the loan will be approved. The period varies with the lender, but typically anywhere from a month to 90 days—and, in some cases, six months.

For your lender, this process includes making sure the property details check out. A mortgage prequalification is like a preapproval, but it may not be as accurate. With a prequalification, you won’t have to provide as much information about your finances, and your lender won’t pull your credit.

How does getting preapproved for a car or mortgage loan work?

One of the biggest advantages of the FHA loan is the smaller down payment requirement. Instead of 20%, you may be able to qualify for a down payment of 3.5%. For example, if you want to buy a home for $250,000, a conventional loan down payment could be $50,000. Add closing costs to that and you could find yourself paying a hefty amount up front for your home. However, an FHA loan at 3.5% means your down payment would only be $8,750. FHA loans often have less stringent credit requirements, so if you have some negative items in your credit history—like a foreclosure or repossession—you may still qualify for an FHA mortgage.

The short answer to whether pre-qualified is the same as pre-approved is, not really, and here’s why. And yes, they both provide a preliminary dollar estimate a borrower may qualify to receive toward a purchase. Within this time period, all credit inquiries related to pre-approvals will be consolidated into a single hit to your credit score.

How long does it take to get final approval from underwriter?

You must have served on active duty for at least 90 days during wartime. Speak with your lender about the fees you should expect so that you know how much youll need to pay. Discuss your lifestyle and budget with your lender to determine which mortgage option works best for you. Just as you want to get the best deal on the house you buy, you also want to get the best deal on your home loan.

It's also possible to apply too late for a mortgage preapproval. It typically takes only a few days to generate a preapproval letter, once you've submitted all necessary documentation . If you're self-employed, have a very limited credit history, or if the lender has questions about any of your back-up documentation, however, the process could take as long as two weeks. Gauge your circumstances accordingly, and don't wait to apply for preapproval when you're already rushed to bid on the ideal property. Remember that multiple checks for credit history can negatively affect your credit rating, so you don’t want to have them repeated often. For the same reason, you shouldn’t apply for it until you’re ready to start seriously home shopping.

You can build your credit by opening a starter credit card with a low credit line limit and paying off your bill each month. It could take up to six months for your payment activity to be reflected in your credit score. When you are ready to make offers, a seller often wants to see a mortgage pre-approval and, in some cases, proof of funds to show that you’re a serious buyer.

Buyers benefit by consulting with a lender, obtaining a pre-approval letter, and discussing loan options and budgeting. The lender will provide the maximum loan amount, which will help set the price range for the home shopper. A mortgage pre-qualification can be useful as an estimate of how much someone can afford to spend on a home, but a pre-approval, often valid for 60 to 90 days, is more valuable. It means the lender has checked the buyer's credit, verified assets, and confirmed employment to approve a specific loan amount. While this may cause your credit score to drop slightly, getting preapproved won’t hurt your credit in a significant way. Subsequent inquiries from other mortgage lenders within the same time period won’t affect your score at all.

But they are often used interchangeably, so be sure your lender is actually going through the pre-approval process if that’s what you intended. Also helps you show real estate agents and sellers that you’re serious about buying. In a competitive market, offers with a pre-approval letter included can stand out among the competition.

The VA’s role in the loan process is to fund and manage the program and be sure it runs smoothly, they do not issue the loans themselves, that is left to the mortgage lenders. Although VA does not require a minimum credit score, but VA lenders generally prefer score of at least 620. While your credit score and the size of your down payment matter, don’t underestimate the value of stable employment.

No comments:

Post a Comment